Introduction

Choosing between sole trader vs limited company is one of the first major decisions many UK founders, freelancers, startups and small business owners need to make. It affects how you pay tax, how much admin you take on, how your business is perceived, how protected your personal finances are and how easy it may be to grow in the future.

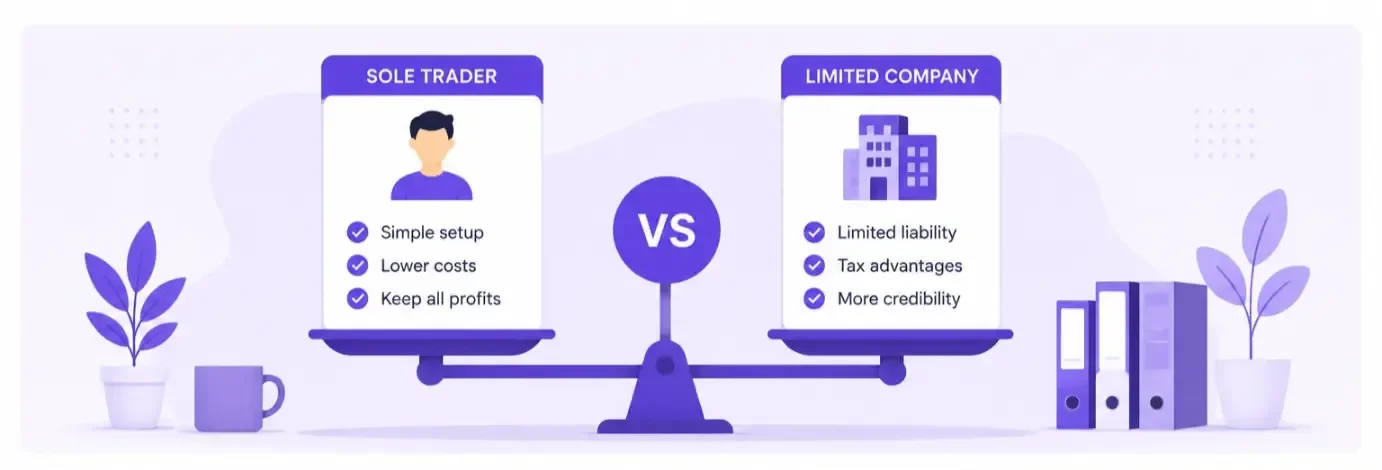

For many new business owners, the question starts simply: should I be a sole trader or limited company? At first glance, becoming a sole trader can feel easier because there is less setup, fewer reporting duties and a more straightforward way to start trading. You can test an idea, invoice clients and manage your own tax affairs without creating a separate legal company. That simplicity is one of the biggest sole trader benefits, especially for side hustles, freelancers and early-stage founders who want to keep costs low.

A limited company, however, can offer advantages as your business becomes more serious. It creates a separate legal identity, can improve credibility with clients, may provide more flexibility around salary and dividends, and can help protect personal assets if the business runs into difficulty. For startups with growth plans, investors, employees, commercial contracts or higher profit potential, a limited company is often seen as the best business structure for startups.

This guide is written for UK sole traders, freelancers, SMEs, startup founders and anyone deciding whether to operate as a sole trader or limited company in 2026. It explains the practical differences in plain English, including tax, liability, setup costs, admin, banking, accounting, credibility, funding and long-term growth.

This article also includes a section on Tide’s company formation product, where eligible users can register a business for £14.99 and potentially earn up to £200 cashback. Offers are subject to eligibility, usage conditions and change, so always check the latest terms before applying. You can view the offer here: https://startupdeals.co.uk/recommends/tide-company-formation

By the end, you should have a clearer view of the best business structure for startups and small businesses, plus a practical framework to decide whether you should stay simple as a sole trader or form a limited company for greater structure and growth potential.

Contents:

What Is a Sole Trader?

What Is a Limited Company?

Sole Trader vs Limited Company: Key Differences Explained

Setup and Registration: Which Is Easier?

Tax Differences Between Each Structure

Liability and Personal Risk

Costs, Admin and Accounting Responsibilities

Credibility and Client Perception

Profit, Growth and Funding Potential

Tide Company Formation Offer for New Limited Companies

Who Should Choose Sole Trader?

Who Should Choose Limited Company?

General FAQs

Recap

Conclusion

What Is a Sole Trader?

A sole trader is one of the simplest ways to run a business in the UK. As a sole trader, you trade as an individual rather than through a separate company. This means you personally own and operate the business, keep the profits after tax, and take responsibility for any losses, debts or legal obligations connected to the business.

For many people starting out, this is the most natural first step. If you are a freelancer, consultant, tradesperson, creator, virtual assistant, designer, tutor, coach or side-hustle owner, registering as a sole trader can be a straightforward way to begin. You do not need to create a company through Companies House. Instead, you normally register for Self Assessment with HMRC when required and report your business income through a tax return.

One of the main sole trader benefits is simplicity. You can start quickly, keep your records relatively straightforward and avoid some of the formal reporting duties that come with running a limited company. This can make sole trader status appealing if you are testing a business idea, earning modest income, working alone or unsure whether the business will become a long-term venture.

However, the simplicity comes with trade-offs. A sole trader and the business are legally the same person. If the business owes money, faces a legal claim or cannot pay a supplier, you may be personally responsible. This does not mean sole trader status is automatically unsafe, but it does mean you need to think carefully about risk, contracts, insurance and the type of work you do.

Another important point is tax. Sole traders pay tax on business profits as personal income. That can be perfectly suitable for smaller businesses, but as profits grow, the question of sole trader or limited company becomes more important. A limited company may offer more flexibility around how profits are retained or withdrawn, although it also brings more admin and compliance.

For startups, sole trader status often works best when the business is simple, low-risk and owner-operated. It can be an excellent starting point for people who want to move quickly without overcomplicating things. But if you are aiming to build a scalable brand, bring in investors, hire staff or protect your personal position, you may eventually need to ask: should I be a sole trader or limited company?

What Is a Limited Company?

A limited company is a separate legal entity from the person or people who own and run it. This means the company exists in its own right. It can enter contracts, own assets, invoice customers, pay tax, open a business bank account and take on liabilities separately from its directors and shareholders.

In the UK, most small businesses that incorporate use a private company limited by shares. This structure is common for startups, agencies, ecommerce businesses, consultants, contractors, software companies and growing SMEs. You register the company with Companies House and normally manage your company tax obligations separately from your personal tax affairs.

The biggest difference from being a sole trader is separation. As a director, you are responsible for running the company properly, but the company itself is usually responsible for its own debts. This is why limited company status can appeal to founders who want to protect their personal assets, take on larger contracts or create a more formal business structure.

A limited company can also create a stronger impression with clients, lenders, suppliers and partners. Some organisations prefer working with limited companies because they look more established and may be easier to verify through public company records. For a startup trying to win business-to-business contracts, this can be helpful.

However, a limited company is not automatically better for everyone. There is more administration. You need to keep company records, maintain accurate accounts, file confirmation statements, submit company tax returns and manage director responsibilities. Many company owners use an accountant or accounting software to stay compliant.

Tax is another key reason people compare sole trader or limited company. A limited company pays Corporation Tax on profits, and directors may take income through salary and dividends depending on their circumstances. This can create planning opportunities for some business owners, particularly when profits begin to increase.

For many founders, a limited company becomes more attractive when the business is profitable, higher-risk or growth-focused. If you are researching the best business structure for startups, a limited company often provides more flexibility for scaling, raising finance and building a recognisable brand. Still, the right choice depends on your income, risk level, admin tolerance and long-term goals.

Sole Trader vs Limited Company: Key Differences Explained

When comparing sole trader vs limited company structures, the decision usually comes down to five key areas: legal separation, tax, administration, financial risk and long-term growth potential. While both structures allow you to operate a legitimate business in the UK, they work very differently in practice.

The biggest distinction is legal identity. A sole trader and the business are considered the same legal entity. This means all profits belong directly to the owner, but so do any debts or liabilities. A limited company, on the other hand, exists separately from the individual running it. The company itself is responsible for contracts, debts and legal obligations in most circumstances.

This legal separation is one of the main reasons many founders eventually move from sole trader to limited company status. If your business begins taking on larger projects, hiring staff or dealing with higher-value contracts, the added protection can become more important.

Tax is another major factor. Sole traders pay Income Tax and National Insurance on profits through Self Assessment. A limited company pays Corporation Tax on profits, while directors normally take money through salary, dividends or a combination of both. Depending on profit levels, this can sometimes create more tax planning flexibility.

However, tax should not be the only reason for incorporation. Some people become too focused on potential tax savings without considering the added responsibilities that come with running a company. A limited company requires more bookkeeping, reporting and compliance work. There are annual accounts, confirmation statements and separate company finances to manage.

Administration is often where sole trader benefits become most obvious. Sole traders generally have fewer filing obligations, simpler accounting and lower setup costs. For freelancers, creatives, consultants and side hustles, this simplicity can be extremely valuable during the early stages of trading.

Credibility can also differ. Although many sole traders run highly successful businesses, some clients and suppliers perceive limited companies as more established or professional. This can matter when approaching larger organisations, applying for finance or building partnerships.

Another key difference is ownership flexibility. A sole trader business belongs entirely to one person. A limited company can have multiple shareholders, directors and investors. This makes it more suitable for businesses with expansion plans or co-founders.

For many startups, the question is not simply sole trader or limited company, but which structure best matches current goals. Someone testing a low-risk side hustle may benefit from staying a sole trader initially. A startup aiming for rapid growth, outside investment or staff recruitment may prefer the structure of a limited company from day one.

Ultimately, the best business structure for startups depends on income levels, future plans, operational risk and personal preference. There is no universal answer. The right structure is the one that supports your business both now and as it develops over time.

Setup and Registration: Which Is Easier?

For many new founders, simplicity matters. When deciding between sole trader vs limited company, setup and registration requirements are often among the first things people compare. The good news is that both structures are relatively accessible in the UK, although the process and responsibilities are quite different.

Starting as a sole trader is generally the easier option. In many cases, you can begin trading almost immediately using your own name or a chosen business name, provided it follows UK naming rules. There is no formal incorporation process and no requirement to register with Companies House. Instead, you normally register for Self Assessment with HMRC when your trading income reaches the relevant threshold or when required by tax rules.

This is one of the strongest sole trader benefits. The lower barrier to entry allows people to test business ideas quickly without committing to the structure and compliance obligations of a limited company. Many freelancers, ecommerce sellers, contractors and creators choose this route because they can begin earning income with minimal administration.

A limited company requires more formal setup. You must register the company through Companies House, choose a company name, appoint at least one director and provide a registered office address. You will also need to issue shares and create company records. While the process itself is usually straightforward online, it involves more decisions and ongoing responsibilities than sole trader registration.

This is where company formation providers can help simplify the process. Services such as Tide’s company formation package are designed to help founders register a business quickly while also accessing a business bank account and startup support features.

Eligible users can register a company through Tide from £14.99 and potentially earn up to £200 cashback, subject to eligibility and promotional conditions. This can be appealing for founders who have already decided that a limited company is the best business structure for startups with long-term ambitions.

You can view the Tide company formation offer here: https://startupdeals.co.uk/recommends/tide-company-formation

Another important difference involves financial separation. Sole traders can legally use a personal bank account for business purposes in some cases, although a separate business account is usually recommended. Limited companies should operate separate company finances because the business is legally distinct from the owner.

If you are asking should I be a sole trader or limited company, setup complexity alone should not make the decision for you. While sole trader registration is easier initially, many businesses later transition to limited company status as they grow. Others remain sole traders for years because the structure continues to suit their needs.

The key is balancing simplicity against long-term goals. If your focus is speed, low admin and testing a business concept, sole trader status may work well. If you want a more formal structure from the beginning, a limited company may provide stronger foundations for growth.

Tax Differences Between Each Structure

Tax is one of the biggest reasons people compare sole trader vs limited company structures. While both types of business must pay tax legally and accurately, the way profits are taxed differs significantly. Understanding these differences can help founders decide which structure is more suitable for their income level and future plans.

A sole trader pays tax on business profits through Self Assessment. After allowable business expenses are deducted, the remaining profit is treated as personal income. This means the business owner pays Income Tax and National Insurance based on current personal tax thresholds and rates.

One of the main sole trader benefits is simplicity. Tax reporting is generally easier to understand, especially for people running smaller businesses or earning modest profits. There is usually less paperwork involved compared with a limited company, and some founders prefer having straightforward visibility over their income.

However, as profits increase, the question of sole trader or limited company often becomes more important. Higher profits can push sole traders into higher Income Tax bands, which may reduce overall tax efficiency. At this stage, some business owners consider incorporating to create more flexibility around how profits are extracted.

A limited company pays Corporation Tax on company profits. Directors can then pay themselves through salary, dividends or a combination of both. Depending on the circumstances, this can sometimes reduce overall tax liability compared with operating as a sole trader, although the difference varies based on profit levels and tax rules.

Retaining profits within the company is another advantage for some businesses. A limited company can leave money inside the business for future growth, investment or cash flow management. Sole traders are taxed on profits regardless of whether the money is withdrawn personally.

That said, limited company taxation is more complex. Directors may need payroll systems, dividend documentation and more detailed accounting support. Many limited companies work with accountants to ensure compliance and tax efficiency.

VAT obligations can also apply to both structures depending on turnover and activities. Whether you are a sole trader or limited company, VAT registration rules generally follow the business rather than the structure itself.

If you are wondering should I be a sole trader or limited company purely for tax reasons, it is important to look beyond headline percentages. Administration costs, accounting fees, future plans and business risk all matter too.

For early-stage founders with lower profits, the simplicity of sole trader taxation may outweigh potential savings from incorporation. For profitable or growing businesses, a limited company may offer more flexibility and scalability over time.

The best business structure for startups is not always the one with the lowest immediate tax bill. It is the structure that supports sustainable growth while remaining manageable and compliant.

Liability and Personal Risk

One of the most important differences in the sole trader vs limited company debate is personal liability. While tax and admin often receive most of the attention, protecting personal finances can be just as important when choosing the right structure.

As a sole trader, you and the business are legally the same entity. This means you personally keep the profits, but you are also personally responsible for debts, financial obligations and certain legal claims connected to the business. If the business cannot pay suppliers, loans or compensation claims, your own assets could potentially be at risk.

This does not automatically make sole trader status dangerous. Many low-risk businesses operate successfully as sole traders for years. Freelancers, consultants, tutors, creators and service-based businesses often prefer this structure because of its simplicity and lower administrative burden. In these situations, the sole trader benefits may outweigh the additional risk.

However, the level of risk depends heavily on the type of business you run. If your work involves physical products, employees, large contracts, client disputes or financial liabilities, personal exposure becomes more important. This is often where founders begin asking themselves: should I be a sole trader or limited company?

A limited company creates legal separation between the owner and the business. The company itself is normally responsible for its debts and obligations. In many cases, directors are protected from personal liability beyond the value of their shares or guarantees they have personally signed.

This limited liability protection is one of the main reasons many growing startups choose incorporation early. It can help reduce personal financial exposure and create a more structured framework for business operations.

That said, limited liability is not absolute. Directors still have legal responsibilities and can become personally liable in certain circumstances, such as fraud, wrongful trading or serious negligence. Running a limited company responsibly remains essential.

Insurance is another important factor regardless of structure. Professional indemnity insurance, public liability insurance and cyber insurance may all be relevant depending on your industry. Even with limited company protection, insurance remains a key part of risk management.

Business credibility can also connect to liability. Some clients feel more comfortable working with limited companies because they appear more established and structured. This can be particularly relevant for agencies, contractors and startups working with corporate clients.

If you are comparing sole trader or limited company status, think realistically about the level of commercial risk involved in your business. A side hustle selling digital templates may carry very different risks from a construction company or ecommerce brand holding inventory.

For many founders, the best business structure for startups depends partly on balancing simplicity with protection. Sole trader status may work perfectly for lower-risk operations, while limited companies often become more attractive as exposure, turnover and business complexity increase.

Costs, Admin and Accounting Responsibilities

When deciding between sole trader vs limited company, many founders underestimate how much ongoing administration can influence their experience of running a business. While tax efficiency and liability matter, day-to-day workload is often what people notice most once trading begins.

A sole trader structure is generally easier and cheaper to manage. This is one of the biggest sole trader benefits for freelancers, side hustles and first-time business owners. Record keeping is usually simpler, filing requirements are lighter and there is less formal administration overall.

As a sole trader, you normally track income and expenses, submit a Self Assessment tax return and keep accurate financial records. Many people manage this themselves using accounting software, spreadsheets or a basic bookkeeping system. Accountancy costs are often lower because the reporting requirements are more straightforward.

This simplicity allows founders to focus more on winning customers and building revenue instead of handling company compliance. For smaller businesses with modest turnover, this can be a major advantage.

A limited company, however, comes with significantly more administration. You must maintain company records, file annual accounts, submit confirmation statements, manage Corporation Tax filings and separate personal finances from business finances. Directors also have legal duties regarding how the company is operated.

Because of these additional responsibilities, many limited companies hire accountants or use advanced accounting software from the beginning. While this can improve financial organisation and tax planning, it also increases running costs.

Banking is another consideration. Sole traders can sometimes begin with a personal account, although a dedicated business account is usually recommended for organisation and professionalism. Limited companies should always use a separate company bank account because the company is legally distinct from the owner.

Payroll can also become more complex with a limited company. Directors taking salaries may need PAYE registration and payroll reporting. Dividend payments also require proper documentation and bookkeeping records.

Despite the added workload, many founders still prefer a limited company because of the structure it provides. As businesses grow, better financial separation and reporting can support scaling, funding applications and long-term planning.

This is particularly relevant for startups with ambitious growth goals. If you are researching the best business structure for startups, the additional administration of a limited company may feel worthwhile if it supports future expansion.

However, not every business needs that level of structure immediately. If your operation is small, low-risk or experimental, the lighter admin of sole trader status can make life significantly easier.

When asking should I be a sole trader or limited company, think carefully about how much administration you are realistically prepared to manage. Some founders value simplicity above all else. Others prefer formal systems that can scale alongside the business.

There is no universally correct answer. The right structure depends on your income, growth plans, industry and tolerance for ongoing compliance responsibilities.

Credibility and Client Perception

Credibility can play a surprisingly important role when choosing between sole trader vs limited company structures. While the legal and tax differences are often more obvious, the way customers, suppliers and partners perceive your business can also influence long-term success.

A sole trader can absolutely operate a professional and successful business. Many experienced consultants, creatives, tradespeople and freelancers choose to remain sole traders because the structure suits their working style and income level. In fact, some clients care far more about quality of service than business structure.

That said, a limited company can sometimes create a stronger impression, particularly in business-to-business environments. Some organisations prefer dealing with incorporated businesses because they appear more established, formal and scalable. For startups targeting larger contracts or corporate clients, this perception can matter.

This is one reason many founders eventually move from sole trader to limited company status as the business grows. Even when tax savings are modest, the professional image associated with incorporation may help support expansion.

A limited company name also appears on the public Companies House register, which can create additional transparency and legitimacy. Clients can verify the business, view registration details and confirm the company exists officially. Some lenders, suppliers and procurement departments may feel more comfortable working with registered companies for this reason.

Branding can also become easier with a limited company. Operating under a registered company name can help create a more distinct business identity, particularly if you plan to build a recognisable brand rather than operate purely under your own personal name.

However, credibility is not solely determined by incorporation. A sole trader with a professional website, branded email address, strong customer reviews and excellent communication may appear more trustworthy than a poorly managed limited company.

This is why the decision should not be based purely on appearances. If you are asking should I be a sole trader or limited company, focus first on what the business actually needs operationally and financially.

Still, perception can influence opportunities. Some larger clients automatically prefer limited companies when awarding contracts. Certain industries also treat incorporation as a sign that the business is serious about long-term operations.

For startups looking to raise finance or attract investors, a limited company is usually the more practical option. Investors generally expect formal share structures and legal separation, both of which are built into the limited company model.

When evaluating the best business structure for startups, credibility should therefore be considered alongside tax, admin and liability. A limited company may strengthen business perception in certain markets, while sole trader status may remain perfectly suitable for lean, independent or service-focused operations.

Ultimately, professionalism comes from how the business is run. Structure can support credibility, but consistency, customer service and reliability matter far more in the long run.

Profit, Growth and Funding Potential

Growth potential is one of the biggest reasons founders compare sole trader vs limited company structures. While both can support profitable businesses, the ability to scale, raise funding and build long-term value often differs significantly between the two.

A sole trader structure can work extremely well for independent professionals and lifestyle businesses. Many freelancers, consultants and service providers generate strong incomes without ever incorporating. One of the major sole trader benefits is flexibility. You can operate leanly, make quick decisions and avoid the administrative layers that often come with a limited company.

For businesses with modest growth ambitions, this simplicity may be ideal. If your goal is stable income, independence and manageable overheads, sole trader status can remain effective for years.

However, growth often changes the equation. As revenue increases, businesses typically become more complex. You may begin hiring staff, outsourcing work, investing in marketing or taking on larger contracts. At this stage, founders frequently revisit the question: should I be a sole trader or limited company?

A limited company is generally better suited to scaling because it creates stronger operational structure. The separation between the business and the owner can improve organisation, financial management and long-term planning. It can also make the business easier to sell, transfer or expand in future.

Funding is another important factor. Sole traders can still access loans and certain types of finance, but investors usually prefer limited companies because they allow ownership to be divided into shares. This creates clearer legal frameworks for investment and equity agreements.

For startups with ambitions to raise capital, attract co-founders or scale rapidly, a limited company is often considered the best business structure for startups. Venture capital firms, angel investors and many lenders typically expect formal company structures before investing.

Retaining profits can also support growth. A sole trader is taxed personally on profits regardless of whether the money is withdrawn. A limited company may allow profits to remain inside the business for reinvestment, potentially improving cash flow and expansion planning.

Recruitment can become easier too. Employees may view limited companies as more stable or established, particularly in competitive industries. Share options and formal employment structures are also generally easier to implement through a company.

That said, not every business needs aggressive growth. Many founders intentionally choose smaller, simpler operations because they value flexibility and independence more than scaling quickly. In these situations, sole trader status may remain entirely appropriate.

The decision ultimately depends on your goals. If you want a straightforward business with minimal complexity, sole trader status may suit you perfectly. If you are building a brand with long-term expansion ambitions, incorporation may provide stronger foundations.

When considering sole trader or limited company status, think about where you want the business to be in three to five years rather than only focusing on today. The structure that feels slightly more complex now may become the better option as the business develops.

Tide Company Formation Offer for New Limited Companies

For founders who decide that a limited company is the right option, company formation services can make the setup process significantly easier. Rather than handling everything manually, many startups now use integrated formation providers that combine company registration with business banking and startup tools.

One popular option is Tide’s company formation service, which is designed for UK startups, freelancers and small businesses wanting to launch quickly with a professional structure.

Eligible users can register a limited company from £14.99 and potentially earn up to £200 cashback, subject to eligibility criteria, promotional conditions and account usage requirements. Offers may change over time, so it is important to check the latest details before applying.

You can view the offer here: https://startupdeals.co.uk/recommends/tide-company-formation

For many founders researching sole trader vs limited company options, setup cost is one of the main concerns. Historically, company formation could feel expensive or overly complicated. Modern formation platforms have simplified this considerably, making incorporation more accessible to startups and first-time business owners.

The Tide package is particularly relevant for founders who have already decided that a limited company is the best business structure for startups with growth ambitions. Instead of managing registration, banking and onboarding separately, the process can often be streamlined through a single platform.

Typically, the service involves registering your company with Companies House while also helping you access a business current account. This can be especially useful because limited companies should operate with separate business finances from the beginning.

To qualify for the current cashback offer, eligible users must use the code STARTUP200 when registering their business and opening a Tide account. You must spend at least £100 on your Tide card within 30 days to unlock the initial £75 cashback reward.

In addition, users who deposit at least £5,000 into a Tide Instant Saver Account within 7 days of opening the account — and keep the funds there for one month — may qualify for an additional £125 cashback reward.

Eligibility usually depends on factors such as being a new customer, meeting account verification requirements and completing qualifying actions linked to the promotion. Cashback offers and eligibility rules may change, so always review the latest terms before applying.

This type of offer is generally more relevant for founders committed to incorporation rather than those still testing an idea casually. If you remain uncertain about sole trader or limited company status, it may be worth evaluating your expected income, business risk and long-term plans first before forming a company.

That said, many startups choose incorporation early because they want stronger branding, liability protection and scalability from day one. A formation offer can help reduce some of the upfront friction involved in making that transition.

If you are asking should I be a sole trader or limited company, the answer may partly depend on where you expect the business to go over the next few years. Founders planning to grow a team, seek investment or build a larger brand often lean towards incorporation sooner rather than later.

While no formation service can decide the right structure for you, simplified setup tools can make the process less intimidating for new business owners ready to launch a limited company.

Who Should Choose Sole Trader?

A sole trader structure is often best suited to people who want simplicity, flexibility and low administrative overheads. For many new founders, it provides the easiest way to begin earning income without immediately taking on the complexity of running a limited company.

Freelancers are one of the clearest examples. Designers, writers, photographers, consultants, coaches and virtual assistants frequently operate successfully as sole traders because their businesses are relatively low-risk and service-based. In these cases, the sole trader benefits can outweigh the advantages of incorporation, particularly during the early stages.

Side hustles are another strong fit. If you are testing a business idea alongside employment, running a small ecommerce operation or monetising a skill part-time, sole trader status can provide a quick and practical entry point into self-employment.

The lower setup burden is a major advantage. You can usually start trading quickly, manage your own records more easily and avoid many of the reporting responsibilities associated with a limited company.

Cash flow can also be simpler. Because the business and owner are legally the same, profits belong directly to you after tax obligations are met. Some founders prefer this straightforward arrangement rather than managing salaries, dividends and company accounts.

Low-risk businesses are often particularly well suited to sole trader status. If your business does not involve large debts, significant liabilities, employees or complex operations, the additional protection of a limited company may not yet be necessary.

This is why many founders initially choose sole trader status even if they later incorporate. It allows them to validate demand, gain experience and generate income before committing to a more formal structure.

However, there are situations where sole trader status may become less suitable over time. As profits increase, taxes may become less efficient compared with a limited company. Larger contracts, business loans and operational risk can also make legal separation more attractive.

If you are regularly asking should I be a sole trader or limited company, it may be a sign that the business is evolving beyond its original stage.

Still, incorporation is not always essential for success. Many people deliberately keep their business lean and independent for lifestyle reasons. They may value reduced admin, simplicity and personal control more than scalability or investment opportunities.

When comparing sole trader or limited company structures, it is important to remember that there is no pressure to scale aggressively. The best business structure for startups is not necessarily the most complex one. It is the structure that aligns with your goals, workload preferences and level of commercial risk.

For many individuals starting out, sole trader status remains the most practical, flexible and accessible route into business ownership.

Who Should Choose Limited Company?

A limited company is often the preferred structure for founders planning to build a scalable, long-term or higher-growth business. While incorporation involves more administration, many entrepreneurs feel the added protection, credibility and flexibility are worth it as the business develops.

Startups with ambitious growth plans are usually strong candidates for incorporation. If you intend to hire employees, seek investment, raise finance or expand operations over time, a limited company can provide a more suitable framework for growth. This is one reason many founders consider it the best business structure for startups with long-term commercial goals.

Higher-profit businesses may also benefit from a limited company structure. As profits increase, the flexibility of taking income through salary and dividends can sometimes create more efficient financial planning opportunities compared with sole trader taxation. This often becomes an important consideration when founders begin asking should I be a sole trader or limited company?

Businesses operating in higher-risk industries may also prefer incorporation because of the legal separation between the company and the owner. Agencies, ecommerce brands, contractors, construction businesses and firms handling significant client contracts often choose a limited company to help reduce personal financial exposure.

Professional perception can be another advantage. Some clients and suppliers prefer dealing with limited companies because they appear more formal and established. This can help when bidding for larger contracts, approaching corporate clients or building long-term commercial relationships.

Founders planning to work with partners or investors also generally benefit from incorporation. Limited companies allow ownership to be divided into shares, making it easier to structure equity arrangements, onboard co-founders or attract outside investment.

Another reason people choose incorporation is separation between personal and business finances. A limited company encourages clearer bookkeeping, dedicated business banking and more structured financial management. Although this creates additional admin, it can also improve organisation and scalability.

That said, a limited company is not automatically the right choice for every startup. The additional reporting obligations, accounting responsibilities and compliance requirements can feel overwhelming for very small or experimental businesses. Some founders prioritise simplicity and flexibility instead.

This is why sole trader benefits remain attractive for many independent professionals. If your business is small, low-risk and unlikely to scale significantly, sole trader status may still be the more practical option.

However, for founders building something intended to grow substantially over time, a limited company often creates stronger long-term foundations. The structure can support funding, expansion, recruitment and commercial credibility more effectively as the business matures.

Ultimately, deciding between sole trader or limited company status comes down to where you want the business to go. If you are building a scalable startup rather than simply creating self-employment income, incorporation may provide greater flexibility and protection in the future.

General FAQs

What is the main difference between a sole trader and limited company?

The biggest difference in sole trader vs limited company structures is legal separation. A sole trader and the business are legally the same entity, while a limited company exists separately from its owner.

Should I be a sole trader or limited company when starting a business?

If you want simplicity and lower admin, sole trader status may suit you initially. If you plan to scale quickly or protect personal assets, a limited company may be the better option.

What are the main sole trader benefits?

Common sole trader benefits include easier setup, lower administration, simpler tax reporting and reduced accountancy costs for smaller businesses.

Is a limited company more tax efficient?

A limited company can sometimes offer greater tax flexibility, particularly for profitable businesses, although the overall benefit depends on income levels and circumstances.

Can I switch from sole trader to limited company later?

Yes, many founders begin as sole traders before incorporating later as the business grows or becomes more profitable.

Is a limited company better for startups?

For businesses planning to grow, hire staff or seek investment, a limited company is often considered the best business structure for startups.

Do sole traders need a business bank account?

A sole trader can sometimes use a personal account, although a dedicated business account is strongly recommended for organisation and professionalism.

Does a limited company protect personal assets?

In many cases, yes. A limited company creates legal separation between the business and the owner, helping reduce personal financial exposure.

Is accounting more difficult for limited companies?

Yes, limited companies usually have more accounting and compliance responsibilities than sole traders, including annual accounts and Corporation Tax filings.

Can a sole trader employ staff?

Yes, sole traders can hire employees if needed, although employment responsibilities and payroll obligations still apply.

Which structure looks more professional?

Some clients perceive limited companies as more established, although professionalism ultimately depends on how the business operates rather than the structure alone.

What is the best business structure for startups?

The best business structure for startups depends on growth plans, risk level, profitability and operational complexity. Some startups benefit from sole trader simplicity, while others need the scalability of a limited company.

Recap

Choosing between sole trader vs limited company structures depends on how you plan to run and grow your business. Both options can work successfully in the UK, but they offer different advantages depending on your goals, income level and appetite for administration.

For many freelancers, consultants and side hustles, sole trader status remains an attractive option because of its simplicity. The lower setup requirements, easier accounting and reduced compliance obligations are some of the most valuable sole trader benefits, especially during the early stages of trading.

A limited company, however, often becomes more appealing as businesses grow. The added legal separation, stronger credibility and greater scalability can make incorporation the best business structure for startups with long-term ambitions. Businesses expecting higher profits, larger contracts or external investment frequently prefer this route.

There is no universal answer to the question should I be a sole trader or limited company. The right choice depends on your specific circumstances, risk level and future plans.

If you decide a limited company is the right structure, Tide’s company formation offer may help simplify the process. Eligible founders can register a company from £14.99 and potentially earn up to £200 cashback, subject to eligibility and promotional conditions.

You can view the offer here: https://startupdeals.co.uk/recommends/tide-company-formation

The most important thing is choosing a structure that supports your business both now and in the future. Many founders begin as sole traders before incorporating later, while others choose a limited company from day one to support long-term growth.

Conclusion

Deciding between sole trader vs limited company status is one of the most important early decisions a UK business owner can make. The structure you choose affects tax, liability, accounting, credibility and the way your business grows over time.

For some founders, the simplicity of sole trader status is exactly what they need. The lower admin burden, easier setup and straightforward tax reporting make it ideal for freelancers, side hustles and low-risk businesses. These sole trader benefits can help new entrepreneurs start quickly without becoming overwhelmed by compliance responsibilities.

For others, a limited company provides stronger long-term advantages. Legal separation, improved scalability, potential tax flexibility and greater credibility can make incorporation the better option for growth-focused businesses. This is especially true for founders building brands, hiring teams or planning to seek investment in the future.

If you are still asking should I be a sole trader or limited company, try focusing on your long-term vision rather than only immediate convenience. Think about expected profits, operational risk, client type and future expansion plans. The best business structure for startups is usually the one that aligns most closely with where the business is heading over the next several years.

It is also important to remember that your decision is not permanent. Many successful businesses begin as sole traders before transitioning into limited companies later as circumstances change.

If you are ready to incorporate, Tide’s company formation offer can help simplify the process. Eligible founders can register a company from £14.99 and potentially earn up to £200 cashback, subject to eligibility and offer conditions. Use the code STARTUP200 at checkout to be eligible for the reward.

You can get started here: https://startupdeals.co.uk/recommends/tide-company-formation

Ultimately, there is no single correct answer in the sole trader or limited company debate. The best choice is the one that balances simplicity, protection, flexibility and growth potential for your specific business journey.

Latest Posts:

- Hoxton Mix vs Virtually There: Which Virtual Office Service Is Better?

Introduction If you’re comparing Hoxton Mix vs Virtually There, you’re likely searching for a virtual office provider that offers the right balance of professionalism, affordability, and flexibility. Whether you’re launching… Read more: Hoxton Mix vs Virtually There: Which Virtual Office Service Is Better?

Introduction If you’re comparing Hoxton Mix vs Virtually There, you’re likely searching for a virtual office provider that offers the right balance of professionalism, affordability, and flexibility. Whether you’re launching… Read more: Hoxton Mix vs Virtually There: Which Virtual Office Service Is Better? - Hoxton Mix vs Icon Offices: Which Virtual Office Is Better?

Introduction Choosing a virtual office provider can have a significant impact on how your business is perceived, how you manage your mail, and even how effectively you maintain privacy as… Read more: Hoxton Mix vs Icon Offices: Which Virtual Office Is Better?

Introduction Choosing a virtual office provider can have a significant impact on how your business is perceived, how you manage your mail, and even how effectively you maintain privacy as… Read more: Hoxton Mix vs Icon Offices: Which Virtual Office Is Better? - 7 Powerful Benefits of Using a Hoxton Mix Virtual Office Address

Introduction For startups, freelancers, sole traders and growing SMEs, establishing a professional business presence can be challenging. Renting physical office space in London is often expensive, particularly during the early… Read more: 7 Powerful Benefits of Using a Hoxton Mix Virtual Office Address

Introduction For startups, freelancers, sole traders and growing SMEs, establishing a professional business presence can be challenging. Renting physical office space in London is often expensive, particularly during the early… Read more: 7 Powerful Benefits of Using a Hoxton Mix Virtual Office Address - Hoxton Mix Review: Features, Pricing, Pros and Cons Explained

Introduction If you’re searching for an honest and detailed hoxton mix review, you’re likely comparing virtual office providers and trying to decide whether Hoxton Mix offers good value for your… Read more: Hoxton Mix Review: Features, Pricing, Pros and Cons Explained

Introduction If you’re searching for an honest and detailed hoxton mix review, you’re likely comparing virtual office providers and trying to decide whether Hoxton Mix offers good value for your… Read more: Hoxton Mix Review: Features, Pricing, Pros and Cons Explained - Hoxton Mix Virtual Office Discount: Save 10% on Your First 12 Months

Introduction If you’re looking for a professional London business address without the cost of renting physical office space, a Hoxton Mix Virtual Office discount could help you reduce your startup… Read more: Hoxton Mix Virtual Office Discount: Save 10% on Your First 12 Months

Introduction If you’re looking for a professional London business address without the cost of renting physical office space, a Hoxton Mix Virtual Office discount could help you reduce your startup… Read more: Hoxton Mix Virtual Office Discount: Save 10% on Your First 12 Months - Tide Referral Code 2026: Powerful Guide to Claim £200 Cashback with STARTUP200

Introduction If you’re looking for a Tide referral code in 2026, you’re probably searching for the best possible deal before opening a business account. Whether you’re a sole trader, freelancer,… Read more: Tide Referral Code 2026: Powerful Guide to Claim £200 Cashback with STARTUP200

Introduction If you’re looking for a Tide referral code in 2026, you’re probably searching for the best possible deal before opening a business account. Whether you’re a sole trader, freelancer,… Read more: Tide Referral Code 2026: Powerful Guide to Claim £200 Cashback with STARTUP200 - Tide vs High Street Banks: Powerful 2026 Review

Introduction Choosing the right business banking solution is one of the most important decisions a UK business owner can make. Whether you’re a sole trader, freelancer, contractor, startup founder, or… Read more: Tide vs High Street Banks: Powerful 2026 Review

Introduction Choosing the right business banking solution is one of the most important decisions a UK business owner can make. Whether you’re a sole trader, freelancer, contractor, startup founder, or… Read more: Tide vs High Street Banks: Powerful 2026 Review - Tide Business Account for Tradespeople | Powerful Guide 2026

Introduction Running a trade business involves much more than completing jobs and keeping customers happy. Whether you’re a plumber, electrician, builder, carpenter, roofer, landscaper, painter, heating engineer, or general contractor,… Read more: Tide Business Account for Tradespeople | Powerful Guide 2026

Introduction Running a trade business involves much more than completing jobs and keeping customers happy. Whether you’re a plumber, electrician, builder, carpenter, roofer, landscaper, painter, heating engineer, or general contractor,… Read more: Tide Business Account for Tradespeople | Powerful Guide 2026 - Tide Business Account for Amazon Sellers: Powerful Guide 2026

Introduction Running an Amazon business in 2026 requires much more than simply listing products and waiting for sales. Whether you operate a private-label brand, wholesale business, retail arbitrage model, or… Read more: Tide Business Account for Amazon Sellers: Powerful Guide 2026

Introduction Running an Amazon business in 2026 requires much more than simply listing products and waiting for sales. Whether you operate a private-label brand, wholesale business, retail arbitrage model, or… Read more: Tide Business Account for Amazon Sellers: Powerful Guide 2026