Introduction

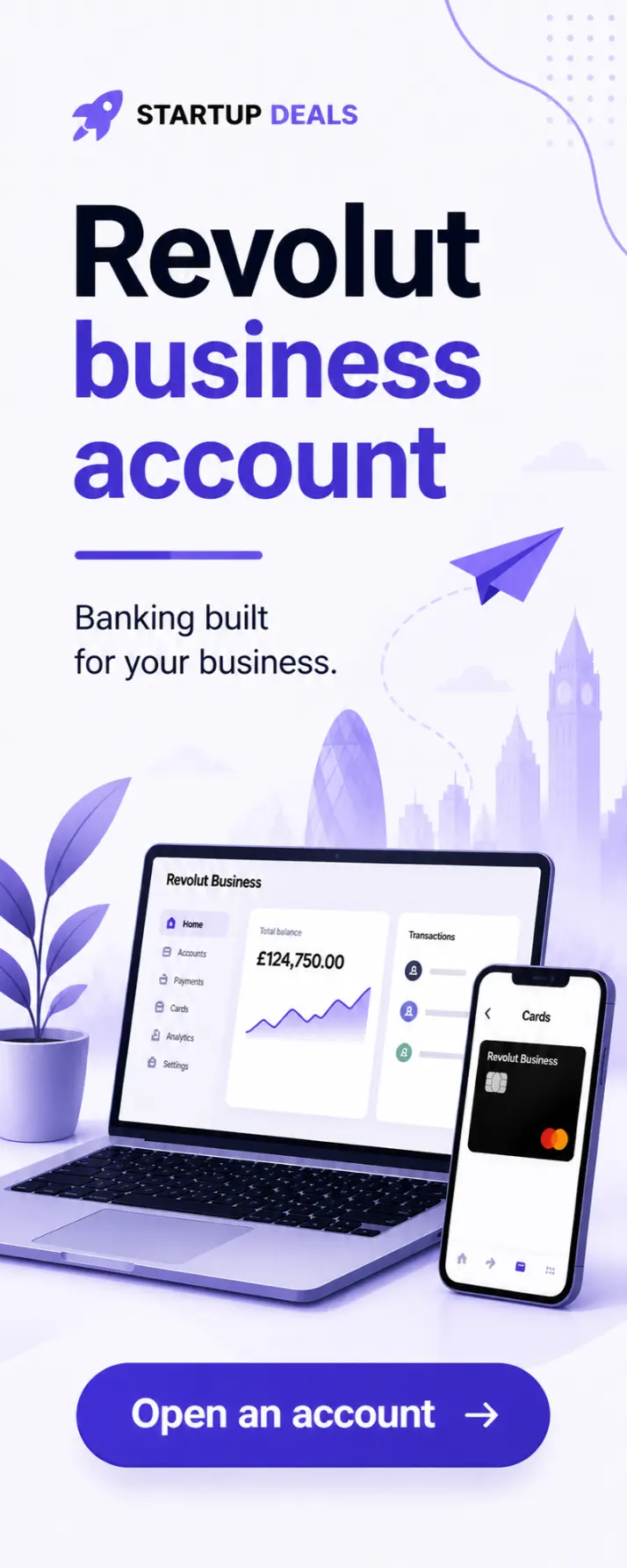

Choosing the right business current account can make everyday finance simpler, cheaper and easier to control. This Revolut business account review is written for UK sole traders, freelancers, startups, founders and SMEs who want a practical, digital-first way to manage payments, cards, expenses, currencies and team spending without relying entirely on a traditional high street bank.

For many small businesses, the problem is not just opening an account. It is finding one that fits how modern businesses actually work. You may invoice clients in pounds, pay suppliers in euros, use contractors abroad, give cards to team members, connect accounting software, track subscriptions and need fast visibility over cash flow. A standard current account can feel limited if your business is international, remote-first or growing quickly.

Revolut Business is designed around that more flexible model. It offers online onboarding, business payments, company cards, multi-currency tools, expense management and integrations depending on the plan you choose. Revolut says UK businesses can apply online, with the application form taking around 10 minutes before review and approval.

This article explains what Revolut Business is, who it suits, where it performs strongly, and where you should compare alternatives before applying. It also covers eligibility, account features, pricing considerations, sole trader suitability, security, common drawbacks and the questions UK business owners usually ask before switching.

Affiliate note: this review may contain an affiliate link. You can apply or learn more through Startup Deals here: https://startupdeals.co.uk/recommends/revolut-business-current-account. Any account approval, pricing, plan benefits or promotional availability is subject to eligibility; offers may change.

A Revolut business account review should not only list features. It should help you decide whether the account matches your day-to-day operations. A freelancer with a few UK clients has different needs from an ecommerce brand taking international payments, while a startup with employees may care more about spend controls, subscriptions and accounting workflows.

So, is this a strong Revolut bank account for small business users in 2026? For the right business, yes. But it is best viewed as a powerful digital finance platform rather than a like-for-like replacement for every traditional banking need. The rest of this guide explains exactly where it fits.

Contents

- Who are Revolut?

- What is a Revolut business account?

- Revolut business account features explained

- Who can open a Revolut Business account in the UK?

- Is a Revolut account suitable for sole traders?

- How to open a Revolut Business account step by step

- Revolut Business pricing and fees

- Revolut Business vs traditional business bank accounts

- International payments and currency tools

- Cards, expenses and team controls

- Accounting integrations and admin tools

- Security, protection and regulation

- General faq’s

- Recap

- Conclusion

Who are Revolut?

Before diving deeper into this Revolut business account review, it helps to understand who Revolut is and how it fits into the UK financial landscape.

Revolut is a UK-founded financial technology company launched in 2015. It started as a digital alternative to traditional banking, focusing on low-cost currency exchange and app-based money management. Since then, it has expanded into a much broader platform offering personal accounts, business accounts, payments, cards, crypto services, and financial tools used by millions of customers globally.

For UK businesses, Revolut operates through its business offering, designed specifically for companies, freelancers and startups. This is important because a Revolut bank account for small business users is not simply an extension of its personal account — it is structured with features like team access, expense controls and multi-user permissions.

One key point in any Revolut business account review is regulation and structure. Revolut is not a traditional high street bank in the UK in the same way as legacy institutions. Instead, it operates as an authorised electronic money institution in the UK, with separate banking licences in some other jurisdictions. This means client funds are safeguarded rather than covered in the same way as deposits in fully licensed UK banks.

In practical terms, safeguarding means your business funds are held separately from Revolut’s own money. However, they are not protected under the Financial Services Compensation Scheme (FSCS) in the same way as deposits in UK banks. For many SMEs and startups, this distinction does not prevent use, but it is something you should clearly understand when deciding if Revolut is a good business account for your needs.

Revolut has grown rapidly due to its focus on speed, design and international functionality. Businesses can apply online, manage everything through an app or desktop dashboard, and access tools that would traditionally require multiple providers. This is why the platform is often considered when evaluating a modern Revolut bank account for small business operations.

From a positioning perspective, Revolut sits somewhere between a traditional bank and a financial software platform. It is particularly strong for digital-first businesses, remote teams and companies that operate across borders. However, it is less focused on in-branch services, lending relationships or cash-heavy operations.

Understanding who Revolut is helps frame the rest of this Revolut business account review. The product is best viewed as a modern finance tool built around flexibility and control, rather than a direct replacement for every feature offered by traditional banks.

What is a Revolut business account?

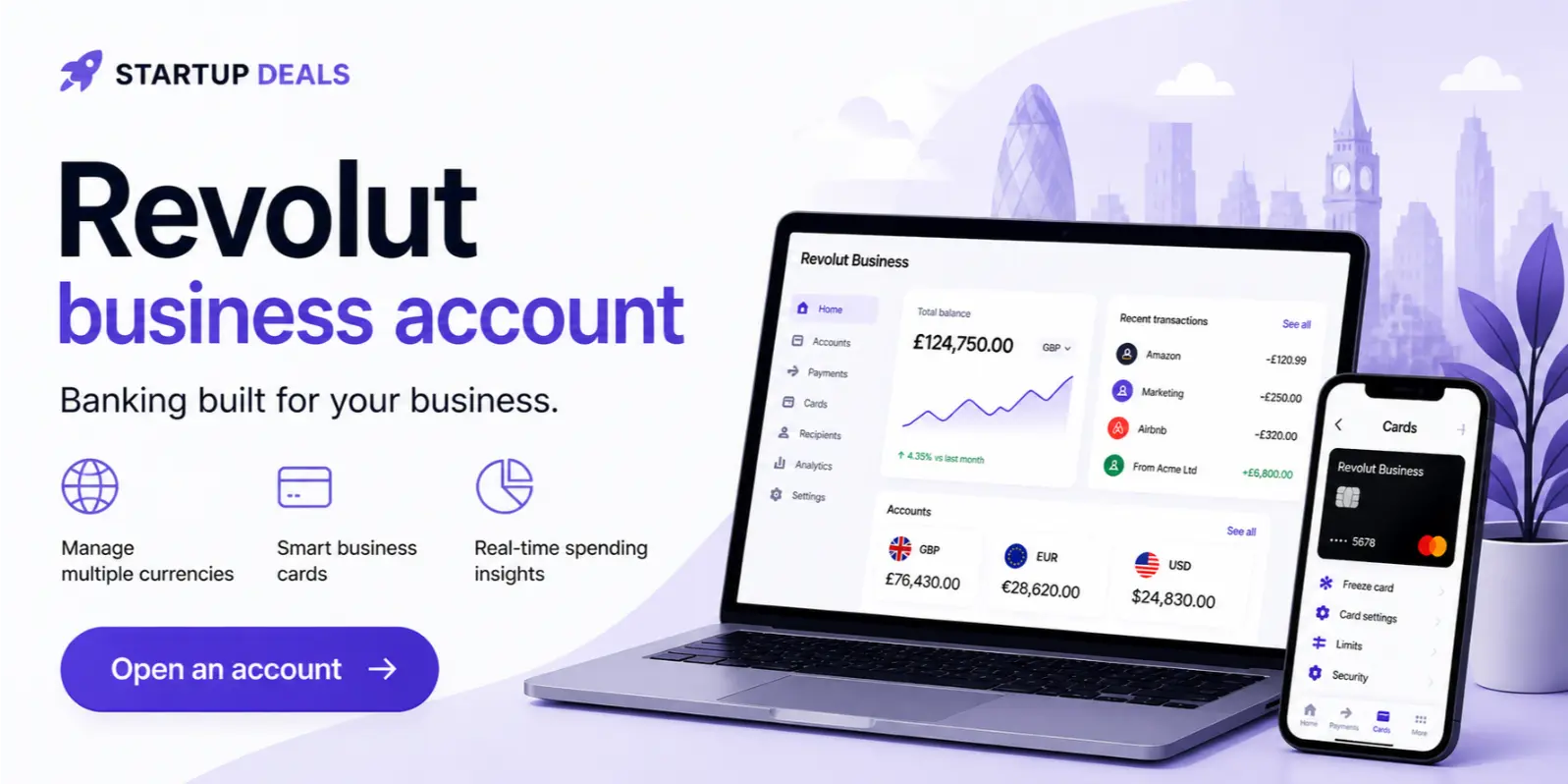

Revolut Business is a digital business current account and financial management platform for companies, freelancers and growing teams. In practical terms, it lets eligible businesses hold money, send and receive payments, issue cards, manage spending, use multiple currencies and organise financial admin from an app or web dashboard.

Revolut describes its Business Account as a current account denominated in pounds sterling, with the option to create sub-accounts in other available currencies in the app. Its business terms state that the account is intended for depositing money, making payments and receiving payments, and must be used for business purposes only.

That distinction matters. This is not a personal account with a business label attached. It is built for commercial use, which means it can support workflows such as team cards, supplier payments, international transfers, payment acceptance and expense controls depending on the plan and features available to your business.

For a small UK company, the appeal is convenience. Instead of managing cards in one place, receipts in another, currency exchange elsewhere and accounting exports manually, Revolut Business brings many of those tasks into one system. This is one reason the product often appears in searches for a Revolut bank account for small business owners who want a faster, more software-led account.

The account is especially relevant for businesses that operate online, trade internationally, use contractors, travel frequently, or want better control over team spending. For example, a startup might issue virtual cards for software subscriptions, while a consultant might use currency accounts to receive overseas client payments. A retailer might value payment acceptance tools, while an agency might care more about expense approval and accounting integrations.

This Revolut business account review also needs to make clear that Revolut Business is plan-based. Revolut currently lists Business plans including Basic, Grow, Scale and Enterprise, with fees and allowances depending on the plan selected. The right plan depends on transaction volume, international payment needs, foreign exchange usage, team size and whether you need advanced controls.

Is Revolut a good business account for every UK business? Not automatically. It can be very strong for digital-first businesses, but businesses that rely heavily on cash deposits, branch support, cheque handling or relationship banking may still prefer a traditional bank alongside it. The best use case is usually a business that values speed, visibility, multi-currency flexibility and modern spend management more than in-branch services.

Revolut business account features explained

The strongest Revolut business account features are built around speed, control and flexibility. Instead of focusing only on storing money, Revolut Business gives owners and finance teams tools to manage how money moves through the business. For many UK SMEs, that is the main reason to consider it over a basic business current account.

Core features include local and international transfers, business cards, currency tools, team access, spending controls, payment acceptance options and expense management. Revolut’s Business site says users can access local and international transfers, payments and expense management tools from the platform. These features make it more than a simple account number and sort code.

The multi-currency side is a major part of the value proposition. Businesses that invoice clients abroad, pay overseas suppliers or hold balances in different currencies may find Revolut useful because it reduces the need to manage several separate accounts. A Revolut bank account for small business users can therefore be particularly attractive for ecommerce, SaaS, consulting, agencies and import/export businesses.

Cards are another important feature. Businesses can typically issue physical and virtual cards, which helps separate spending by employee, subscription, project or department. Virtual cards can be useful for online tools and ad platforms, while physical cards suit travel or in-person purchases. Spending limits and permissions can help founders avoid the common problem of losing track of who spent what and why.

Expense management is also a key part of the account. Rather than waiting until month-end to chase receipts, team members can upload evidence of spending and categorise transactions. This can reduce admin and make bookkeeping smoother. It is one of the reasons this Revolut business account review is especially relevant to founders who want fewer manual finance tasks.

Integrations also matter. Many small businesses already use accounting software, payroll tools, ecommerce platforms or payment services. Revolut Business can help streamline that finance stack, although the exact integrations and features available may depend on your plan, region and account setup.

Is Revolut a good business account if you only need a very simple place to receive UK client payments? It may be, but you should compare the monthly plan cost, transfer allowances and support model against simpler business accounts. Its real strength appears when you use the wider platform: cards, currencies, approvals, expenses and reporting.

Overall, the feature set is best suited to businesses that want finance operations to feel more like modern software. If you value automation, international capability and real-time visibility, the Revolut business account features are compelling. If you mainly need cash deposits and face-to-face support, the fit may be weaker.

Who can open a Revolut Business account in the UK?

Understanding eligibility is a key part of any Revolut business account review, especially if you are deciding whether to apply as a sole trader, limited company or startup. While Revolut aims to make onboarding fast and accessible, not every business will qualify automatically, and requirements can vary depending on structure, activity and location.

In the UK, Revolut Business accounts are generally available to registered businesses, including private limited companies (Ltd), partnerships and some sole traders or freelancers. Your business must be legally registered and operating in a supported country, with the UK being one of Revolut’s core markets. This makes it a realistic option for many founders searching for a Revolut bank account for small business use.

Applicants are usually required to provide standard business information during onboarding. This includes company registration details, business address, nature of activities, and information about directors or beneficial owners. Identity verification is also required, which may involve uploading documents and completing checks digitally. This process reflects standard compliance rules across financial services and is one of the reasons Revolut can offer relatively fast account setup compared to traditional banks.

However, not all industries are accepted. Like most financial providers, Revolut has restrictions on certain business types, particularly those considered high risk. This can include sectors such as gambling, certain financial services, adult services or businesses with complex ownership structures. If your business falls into a restricted category, your application may be declined or require additional review.

Another important factor in this Revolut business account review is operational footprint. Your business should have a genuine presence in the UK or another supported country. This typically means being registered locally and carrying out legitimate commercial activity. Businesses with unclear ownership structures, offshore-only setups or insufficient documentation may face delays or rejection during onboarding.

For startups and newer businesses, Revolut can still be accessible. You do not necessarily need years of trading history to apply, which is why it is often considered when asking “is Revolut a good business account” for early-stage founders. As long as you can demonstrate a legitimate business purpose and meet compliance checks, newer companies can often open an account successfully.

Sole traders and freelancers may also be eligible, although the experience can differ slightly compared to limited companies. This is explored further in the dedicated section on sole trader suitability. Still, the availability of a Revolut bank account for small business users who are self-employed is one of the platform’s strengths.

Finally, approval is not guaranteed. Applications are subject to internal checks, and Revolut may request additional information before granting access. Timelines can vary depending on verification complexity and business type.

In summary, Revolut Business is accessible to a wide range of UK businesses, particularly digital-first companies, startups and SMEs. If your business is legitimate, clearly structured and operates within supported industries, you are likely to meet the core eligibility criteria.

Is a Revolut account suitable for sole traders?

For many self-employed professionals, one of the most important questions in any Revolut business account review is whether the account works well for sole traders. If you are a freelancer, contractor or independent consultant, your financial needs are often simpler than a larger company, but you still need clear separation between personal and business finances.

Revolut does support sole traders in the UK, making it a viable option for those searching for a Revolut bank account for small business use without forming a limited company. This includes freelancers in industries such as design, marketing, consulting, IT services, coaching and ecommerce. As long as you are operating a legitimate business and can pass verification checks, you can usually apply.

One of the main advantages for sole traders is simplicity. Instead of relying on a personal account and manually separating transactions, a Revolut Business account provides a dedicated space for business income and expenses. This can make tax reporting, bookkeeping and financial tracking significantly easier. It is one of the reasons many freelancers ask, “is Revolut a good business account” when trying to professionalise their setup.

The digital-first nature of the platform also suits self-employed users. You can send invoices, receive payments, manage subscriptions and track spending in one place. If you work with international clients, the multi-currency functionality becomes especially useful, allowing you to receive and hold funds in different currencies without constantly converting them.

Another benefit is card flexibility. Sole traders can use physical and virtual cards to manage business spending, which is particularly helpful if you use multiple tools or platforms. For example, you might assign a virtual card to software subscriptions or advertising spend, helping you keep costs organised and easier to review each month.

Expense tracking is also relevant. Instead of storing receipts manually, you can categorise transactions and attach documentation within the platform. This can reduce admin time and simplify communication with your accountant, especially if you integrate with accounting software.

However, this Revolut business account review should also highlight potential limitations for sole traders. If your business relies heavily on cash payments or cheque deposits, Revolut may not be the best standalone solution. It is designed primarily for digital transactions, so traditional banking features may be limited.

Additionally, while Revolut offers strong tools, some sole traders may find the monthly plan structure less appealing if they only need very basic functionality. In that case, comparing it with simpler or free business accounts is sensible.

Overall, a Revolut bank account for small business users who are sole traders can be a strong choice if you value digital tools, international flexibility and streamlined expense management. It is particularly well suited to freelancers and online businesses that want efficiency without the overhead of traditional banking processes.

How to open a Revolut Business account step by step

Opening an account is one of the most practical parts of any Revolut business account review, especially for founders who want to move quickly. Revolut is designed to streamline onboarding compared to traditional banks, but there are still clear steps you need to follow to get approved and start using the account.

Below is a step-by-step guide to applying for a Revolut bank account for small business use in the UK.

Step 1: Start your application online

Go to the official Revolut Business website or apply via a partner link such as: https://startupdeals.co.uk/recommends/revolut-business-current-account

You will begin by entering basic details about your business, including your company name, registration type and country. This initial stage is quick and designed to confirm that your business is eligible to proceed.

Step 2: Provide business information

Next, you will be asked to submit more detailed information about your business. This typically includes:

- Registered company name and number (if applicable)

- Business address and contact details

- Nature of your business activities

- Expected transaction volumes and currencies

This information helps Revolut understand how you intend to use the account and ensures compliance with financial regulations.

Step 3: Verify identity and ownership

Identity verification is a required step. You will need to provide details for directors, shareholders or beneficial owners. This may involve uploading ID documents and completing a verification check through the app or browser.

This stage is standard across financial providers and is one reason why Revolut can approve accounts relatively quickly compared to traditional banks. However, if your structure is more complex, additional checks may be required.

Step 4: Submit documents

Depending on your business type, you may be asked to upload supporting documents such as:

- Certificate of incorporation

- Proof of address

- Business activity evidence (e.g. website or invoices)

For sole traders, this process is usually simpler but may still require proof of identity and business activity.

Step 5: Wait for review and approval

Once everything is submitted, Revolut reviews your application. Approval times can vary. Some businesses are approved quickly, while others may be asked for further information.

This is a key point in any Revolut business account review: approval is not automatic, and timelines depend on verification complexity.

Step 6: Set up your account

After approval, you can access your account dashboard. At this stage, you can:

- Order business cards

- Create currency accounts

- Invite team members

- Set spending controls

- Connect accounting tools

This is where the platform starts to feel more like a financial management system than a traditional bank account.

Step 7: Start using key features

Once set up, you can begin sending and receiving payments, managing expenses and using the tools included in your plan. Many users explore features such as virtual cards, subscriptions tracking and integrations early on.

Is Revolut a good business account from an onboarding perspective? For many UK businesses, yes. The process is faster and more flexible than most high street banks, particularly for digital-first companies.

However, it is still important to ensure your documentation is accurate and complete before applying. Delays usually happen when information is missing or unclear.

Revolut Business pricing and fees

Understanding costs is essential in any Revolut business account review, because pricing can directly affect how suitable the account is for your business model. Revolut Business operates on a tiered plan structure, meaning you typically pay a monthly subscription in exchange for a set of features and usage allowances.

In the UK, Revolut Business generally offers multiple plans, often including entry-level and more advanced tiers designed for growing companies. These plans may include options such as Basic, Grow, Scale and Enterprise, with increasing levels of functionality, limits and support. The right choice depends on how frequently you send payments, whether you deal internationally, and how many team members need access.

At the lower end, plans are designed for smaller businesses or those with lighter usage. These may include a limited number of free transfers, basic expense tools and access to the core platform. As you move up through the tiers, you typically gain higher allowances for transfers, more advanced features, and additional tools such as enhanced expense controls or integrations.

A key cost consideration in this Revolut business account review is transaction-based pricing. While some actions are included within your monthly allowance, additional usage may incur fees. This can include:

- Extra local or international transfers beyond your plan limit

- Foreign exchange transactions above a certain threshold

- Payment acceptance fees (if using merchant tools)

- Card-related costs, depending on usage and type

For businesses that operate internationally, foreign exchange (FX) costs are particularly important. Revolut is known for competitive exchange rates compared to traditional banks, but fees can still apply depending on timing, currency and plan limits. This is why many founders researching a Revolut bank account for small business use compare FX costs carefully.

Another factor is scalability. As your business grows, your financial needs may change. A plan that works well for a freelancer may not suit a team of 10 with frequent international payments. One advantage of Revolut is the ability to upgrade plans as your usage increases, although this also raises your monthly cost.

Is Revolut a good business account in terms of pricing? It depends on how you use it. For businesses that actively use its features—such as multi-currency accounts, team cards and integrations—the value can outweigh the monthly fee. For businesses with minimal activity, the subscription cost may feel less justified compared to simpler or free alternatives.

Transparency is another important point. Revolut provides pricing details within its platform and on its website, but fees can change over time. Always review the latest pricing before applying to ensure it matches your expected usage.

In summary, the Revolut business account features are closely tied to its pricing structure. The more you use the platform’s capabilities, the more value you are likely to extract. However, choosing the right plan and understanding usage limits is essential to avoid unexpected costs.

Revolut Business vs traditional business bank accounts

Comparing providers is a core part of any Revolut business account review, because the real question is not just what Revolut offers, but how it stacks up against traditional UK business bank accounts. For many founders, the decision comes down to digital flexibility versus conventional banking services.

Traditional banks in the UK—such as HSBC, Barclays or NatWest—have long been the default choice for business current accounts. They typically offer branch access, cheque handling, lending relationships and, in many cases, eligibility for FSCS protection on deposits. These features can be important for businesses that rely on cash deposits, in-person support or established credit lines.

By contrast, Revolut Business is built as a digital-first platform. There are no branches, and most interactions happen through the app or web dashboard. For many modern businesses, especially those operating online, this is not a drawback. In fact, it can be a major advantage. Faster setup, real-time spending visibility and integrated tools are key reasons why people consider a Revolut bank account for small business use.

One of the biggest differences lies in functionality. Traditional accounts are often more basic, focusing on storing money, sending payments and providing statements. Revolut goes further by offering features like multi-currency accounts, virtual cards, expense tracking and integrations. This is why the Revolut business account features appeal to startups, ecommerce brands and service-based businesses with distributed teams.

Speed is another differentiator. Opening a traditional business account can take days or even weeks, particularly if manual checks are required. Revolut’s onboarding process is usually faster, although approval is still subject to verification. For startups needing quick access to a business account, this can be a decisive factor when asking “is Revolut a good business account”.

However, traditional banks still have strengths that Revolut does not fully replicate. Cash handling is a major one. If your business regularly deals with physical cash or cheques, a high street bank is likely more practical. Lending is another area—many traditional banks offer business loans, overdrafts and relationship-based financial support that may not be available in the same way through Revolut.

Security and perception also play a role. Some clients or partners may feel more comfortable working with established banks, particularly in industries where traditional banking relationships are the norm. While Revolut is widely used, it still operates differently from legacy institutions, which can influence decision-making for some businesses.

In reality, many UK businesses do not treat this as an either-or decision. Instead, they use Revolut alongside a traditional bank account. For example, a company might use a high street bank for core funds and cash handling, while using Revolut for international payments, cards and expense management.

So, is Revolut a good business account compared to traditional options? It depends on your priorities. If you value digital tools, speed and international flexibility, it can outperform many legacy accounts. If you need in-branch services, lending and cash handling, a traditional bank may still be essential.

International payments and currency tools

One of the strongest reasons businesses explore this Revolut business account review is the platform’s international capability. For UK companies that work across borders, managing multiple currencies efficiently can be a major challenge. Traditional banks often charge higher fees, apply wider exchange rate margins, and make international transfers slower or less transparent.

Revolut Business is built with global transactions in mind. It allows businesses to hold, send and receive money in multiple currencies from within a single account. This is particularly useful for companies with international clients, overseas suppliers or remote teams. Instead of opening separate accounts or relying on third-party services, you can manage everything in one place.

For many founders researching a Revolut bank account for small business use, this multi-currency functionality is a key advantage. You can receive payments in different currencies and choose when to convert them, which gives more control over exchange rates and timing. This can be beneficial if your business income fluctuates based on currency movements.

Speed is another factor. International transfers through traditional banks can sometimes take several days, depending on the destination and intermediary banks involved. Revolut aims to make these transfers faster and more transparent, although exact timings can still vary depending on the currency and payment route.

Foreign exchange (FX) is central to this section of the Revolut business account review. Revolut is known for offering competitive exchange rates compared to many high street banks, particularly within plan allowances. However, it is important to understand that fees may apply outside of those limits or during certain conditions. Businesses that frequently convert large volumes should review the current pricing structure carefully.

Another useful feature is the ability to create named currency accounts within your main account. For example, you can hold euros, US dollars or other supported currencies alongside your GBP balance. This can simplify reconciliation, invoicing and financial reporting, especially for businesses that operate internationally on a regular basis.

Payment tracking and transparency also add value. Being able to see where your money is, when it is expected to arrive and what fees apply can reduce uncertainty and improve cash flow management. This is one reason why many SMEs ask, “is Revolut a good business account” when dealing with cross-border transactions.

That said, there are still considerations. Not all currencies or payment corridors are equal, and fees can vary depending on usage and plan. Additionally, if your business relies heavily on complex international banking arrangements, you may still need supplementary services.

Overall, for businesses that trade internationally, the global capabilities are a standout part of the Revolut business account features. It is particularly well suited to digital businesses, ecommerce operations and service providers working with clients worldwide.

Cards, expenses and team controls

review. For UK businesses with employees, contractors or multiple tools and subscriptions, having clear control over who spends what—and where—can save time, reduce errors and improve financial visibility.

Revolut Business allows you to issue both physical and virtual cards. This is particularly useful for companies that want to separate spending across team members, departments or specific use cases. For example, a marketing team might have its own card for advertising platforms, while a founder keeps a separate card for travel or operational expenses. This level of separation is one of the reasons many founders consider a Revolut bank account for small business use.

Virtual cards are especially valuable in a digital-first environment. You can create cards instantly for online payments, subscriptions or one-off purchases without waiting for physical delivery. This can improve security and organisation, as each card can be assigned a clear purpose. If a subscription is no longer needed, the associated card can simply be frozen or deleted.

Spending controls are another key part of the Revolut business account features. Business owners can set limits on individual cards, restrict where they can be used, and monitor transactions in real time. This reduces the risk of overspending and helps maintain tighter financial discipline, especially in growing teams.

Expense management is closely linked to card usage. Instead of manually tracking receipts and reconciling transactions later, team members can upload receipts and categorise expenses as they happen. This can significantly reduce administrative workload and improve accuracy when preparing accounts or working with an accountant.

Approval workflows can also be implemented depending on the plan. This means certain payments or expenses may require authorisation before they are processed. For businesses scaling beyond a small team, this adds an extra layer of control and accountability.

From a visibility standpoint, everything is centralised. You can see transactions, spending categories and card usage from a single dashboard. This real-time insight is one of the reasons people ask “is Revolut a good business account” for managing day-to-day operations more efficiently.

However, this Revolut business account review should also mention potential limitations. If your business relies on cash payments or traditional expense processes, these digital tools may not fully replace existing workflows. Additionally, some advanced controls or features may only be available on higher-tier plans.

For most modern SMEs, startups and freelancers, the combination of cards, expense tracking and team controls is a strong selling point. It turns the account into an active financial management tool rather than just a place to hold money. This is where Revolut Business often stands out compared to more basic business accounts.

Accounting integrations and admin tool

A key part of this Revolut business account review is how well it fits into your wider financial workflow. Most UK businesses already use accounting software, invoicing tools or ecommerce platforms, so the ability to connect everything efficiently can make a significant difference to day-to-day operations.

Revolut Business offers integrations with popular accounting platforms, helping automate tasks such as transaction syncing, categorisation and reconciliation. Instead of manually exporting statements or entering data line by line, transactions can flow directly into your accounting system. For many founders, this is one of the biggest advantages of using a Revolut bank account for small business use.

This automation reduces the risk of errors and saves time, particularly during month-end or tax preparation. It also makes it easier to work with accountants or bookkeepers, as financial data is more organised and up to date. For businesses managing multiple income streams or high transaction volumes, this can be a major efficiency gain.

In addition to integrations, Revolut provides built-in admin tools designed to simplify financial management. These may include features such as transaction categorisation, reporting dashboards and activity tracking. Having this level of visibility in one place helps business owners understand spending patterns, monitor cash flow and make more informed decisions.

User access controls are another useful feature. You can assign roles and permissions to team members, ensuring that employees only have access to the functions they need. This is particularly helpful for growing businesses where finance responsibilities are shared across a team.

From an operational perspective, these tools support a more streamlined way of working. Instead of juggling multiple systems, businesses can centralise key financial activities within one platform. This is why many people ask, “is Revolut a good business account” when looking to modernise their financial processes.

That said, the level of integration and functionality can vary depending on your plan and specific setup. Some businesses with more complex accounting needs may still rely on additional tools alongside Revolut.

Overall, the combination of integrations and admin features strengthens the Revolut business account features by reducing manual work and improving financial clarity. For digital-first businesses, this can be one of the most valuable aspects of the platform.

Security, protection and regulation

Security is a critical consideration in any Revolut business account review, particularly for UK businesses deciding where to hold and manage their funds. While Revolut offers a modern, digital-first experience, it is important to understand how it protects your money and how it is regulated compared to traditional banks.

In the UK, Revolut operates its business accounts under an electronic money institution (EMI) licence rather than a full UK banking licence. This distinction is important. Instead of holding deposits in the same way as a traditional bank, Revolut safeguards client funds by keeping them separate from its own operational money. These funds are typically held in ring-fenced accounts with established financial institutions.

Safeguarding means that if Revolut were to become insolvent, customer funds should be protected and returned, subject to the safeguarding process. However, unlike many high street banks, balances are not covered by the Financial Services Compensation Scheme (FSCS). This is one of the most commonly asked questions when evaluating whether this is a Revolut bank account for small business use you can rely on long term.

From a practical standpoint, many SMEs and startups are comfortable with this structure, especially when using Revolut as part of a broader financial setup. However, it is something you should factor into your decision, particularly if you plan to hold large balances in the account.

Beyond regulatory structure, Revolut provides a range of in-app security features. These include real-time transaction notifications, card freezing and unfreezing, spending controls and the ability to manage permissions across team members. These tools give business owners direct control over account activity and can help prevent unauthorised use.

Fraud prevention and monitoring systems are also part of the platform. Suspicious transactions may be flagged automatically, and additional verification steps can be required for certain activities. While no system is completely risk-free, these controls align with modern digital banking standards and contribute to overall account security.

Access management is another important area. Businesses can assign roles to team members, limiting who can view, spend or approve transactions. This reduces internal risk and ensures that financial responsibilities are clearly defined.

Is Revolut a good business account from a security perspective? For many digital-first businesses, the answer is yes, particularly due to its real-time controls and visibility. However, the lack of FSCS protection compared to traditional banks remains a key consideration.

Overall, security in Revolut Business combines regulatory safeguarding with practical, user-controlled tools. As part of a balanced financial setup, it can offer a secure and flexible solution for managing business finances.

General FAQs about Revolut

What is a Revolut business account?

A Revolut business account is a digital business finance platform that allows UK companies, freelancers and SMEs to manage payments, cards, expenses and multiple currencies in one place.

Is Revolut a good business account for UK startups?

Yes, many founders consider it a strong option because of its speed, flexibility and modern tools, although whether Revolut is a good business account depends on your specific needs.

Can I use a Revolut bank account for small business transactions only?

Yes, the account is designed strictly for business use, helping separate personal and company finances clearly.

Does this Revolut business account review apply to sole traders?

Yes, this Revolut business account review includes sole traders, freelancers and self-employed users, although features may differ slightly from limited companies.

Are Revolut business account features suitable for international businesses?

Yes, Revolut business account features are particularly strong for international payments, currency management and cross-border transactions.

Is Revolut a good business account for freelancers?

It can be, especially if you need digital tools, expense tracking and multi-currency support as a freelancer or contractor.

Can I hold multiple currencies with a Revolut bank account for small business use?

Yes, one of the key Revolut business account features is the ability to hold and manage multiple currencies within a single account.

How fast is account approval according to this Revolut business account review?

Approval can be quick compared to traditional banks, but it depends on verification checks and business complexity.

Does Revolut offer business debit cards?

Yes, Revolut business account features include physical and virtual cards for spending, subscriptions and team use.

Is Revolut a good business account for managing expenses?

Yes, expense tracking and real-time visibility are key strengths highlighted in most Revolut business account review insights.

Recap

This Revolut business account review has explored how the platform works, who it is for, and where it fits within the UK business banking landscape. For many sole traders, startups and SMEs, Revolut offers a modern alternative to traditional accounts, focusing on speed, flexibility and control rather than in-branch services.

The account is particularly well suited to digital-first businesses. If you operate online, work with international clients, manage subscriptions or need visibility over team spending, the platform delivers strong value. The combination of multi-currency support, card controls, expense tracking and integrations makes it more than just a place to store money. These Revolut business account features position it as a financial management tool rather than a basic current account.

At the same time, it is not a one-size-fits-all solution. Businesses that rely heavily on cash deposits, cheque handling or traditional lending relationships may still need a high street bank alongside it. This is why many UK companies use Revolut in combination with another account rather than as a complete replacement.

When asking “is Revolut a good business account”, the answer depends on how your business operates. For freelancers, ecommerce brands, agencies and startups, it often provides a strong balance of usability and functionality. For more traditional businesses, it may work best as a secondary account.

If you are considering applying, you can explore the latest details here: https://startupdeals.co.uk/recommends/revolut-business-current-account

Conclusion

Choosing the right account comes down to how well it supports your day-to-day operations and future growth. This Revolut business account review shows that the platform is designed for modern businesses that prioritise efficiency, automation and international capability.

The strength of Revolut lies in its ability to combine multiple financial tools into a single system. From payments and currencies to cards and expense management, it offers a streamlined experience that can reduce admin and improve financial visibility. For many UK founders, that alone makes it a compelling option when evaluating a Revolut bank account for small business use.

However, it is important to approach the decision with a clear understanding of your needs. If your business requires traditional banking services such as cash handling or lending, you may need to supplement Revolut with another provider. If your focus is digital operations, global transactions and real-time control, it is likely to be a strong fit.

So, is Revolut a good business account? For the right type of business, absolutely. It delivers flexibility, speed and a feature set that aligns closely with how many SMEs and startups operate in 2026.

If you are ready to explore it further or apply, you can get started here: https://startupdeals.co.uk/recommends/revolut-business-current-account

As always, approval is subject to eligibility, and terms, pricing and features may change—so check the latest details before applying.

Latest Posts:

- Hoxton Mix Review: Features, Pricing, Pros and Cons Explained

Introduction If you’re searching for an honest and detailed hoxton mix review, you’re likely comparing virtual office providers and trying to decide whether Hoxton Mix offers good value for your… Read more: Hoxton Mix Review: Features, Pricing, Pros and Cons Explained

Introduction If you’re searching for an honest and detailed hoxton mix review, you’re likely comparing virtual office providers and trying to decide whether Hoxton Mix offers good value for your… Read more: Hoxton Mix Review: Features, Pricing, Pros and Cons Explained - Hoxton Mix Virtual Office Discount: Save 10% on Your First 12 Months

Introduction If you’re looking for a professional London business address without the cost of renting physical office space, a Hoxton Mix Virtual Office discount could help you reduce your startup… Read more: Hoxton Mix Virtual Office Discount: Save 10% on Your First 12 Months

Introduction If you’re looking for a professional London business address without the cost of renting physical office space, a Hoxton Mix Virtual Office discount could help you reduce your startup… Read more: Hoxton Mix Virtual Office Discount: Save 10% on Your First 12 Months - Tide Referral Code 2026: Powerful Guide to Claim £200 Cashback with STARTUP200

Introduction If you’re looking for a Tide referral code in 2026, you’re probably searching for the best possible deal before opening a business account. Whether you’re a sole trader, freelancer,… Read more: Tide Referral Code 2026: Powerful Guide to Claim £200 Cashback with STARTUP200

Introduction If you’re looking for a Tide referral code in 2026, you’re probably searching for the best possible deal before opening a business account. Whether you’re a sole trader, freelancer,… Read more: Tide Referral Code 2026: Powerful Guide to Claim £200 Cashback with STARTUP200 - Tide vs High Street Banks: Powerful 2026 Review

Introduction Choosing the right business banking solution is one of the most important decisions a UK business owner can make. Whether you’re a sole trader, freelancer, contractor, startup founder, or… Read more: Tide vs High Street Banks: Powerful 2026 Review

Introduction Choosing the right business banking solution is one of the most important decisions a UK business owner can make. Whether you’re a sole trader, freelancer, contractor, startup founder, or… Read more: Tide vs High Street Banks: Powerful 2026 Review - Tide Business Account for Tradespeople | Powerful Guide 2026

Introduction Running a trade business involves much more than completing jobs and keeping customers happy. Whether you’re a plumber, electrician, builder, carpenter, roofer, landscaper, painter, heating engineer, or general contractor,… Read more: Tide Business Account for Tradespeople | Powerful Guide 2026

Introduction Running a trade business involves much more than completing jobs and keeping customers happy. Whether you’re a plumber, electrician, builder, carpenter, roofer, landscaper, painter, heating engineer, or general contractor,… Read more: Tide Business Account for Tradespeople | Powerful Guide 2026 - Tide Business Account for Amazon Sellers: Powerful Guide 2026

Introduction Running an Amazon business in 2026 requires much more than simply listing products and waiting for sales. Whether you operate a private-label brand, wholesale business, retail arbitrage model, or… Read more: Tide Business Account for Amazon Sellers: Powerful Guide 2026

Introduction Running an Amazon business in 2026 requires much more than simply listing products and waiting for sales. Whether you operate a private-label brand, wholesale business, retail arbitrage model, or… Read more: Tide Business Account for Amazon Sellers: Powerful Guide 2026